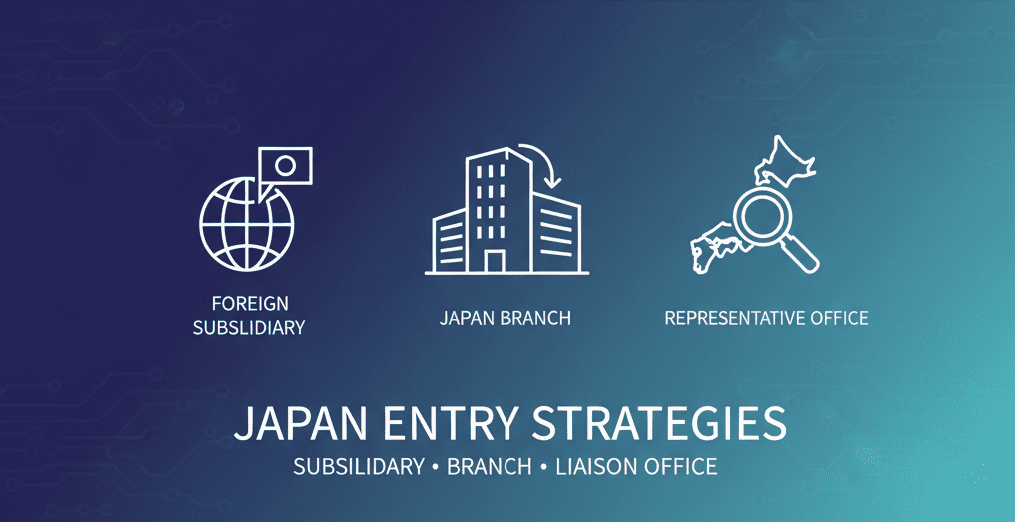

foreign company entry forms in Japan

When foreign companies or foreign nationals plan to enter the Japanese market, the first critical decision they face is “which entry form to choose.” There are three main options: establishing a Japanese corporation, setting up a Japanese branch office, and establishing a representative office. Each option has different advantages and disadvantages, legal positioning, and tax treatment.

This article provides detailed explanations of these entry forms from basic to advanced levels, offering comparative analysis from practical perspectives to help you make optimal choices based on business scale and objectives. We comprehensively explain important points that are often overlooked, including tax differences and legal liability locations.

Three Basic Forms of Foreign Company Entry into Japan

For foreign companies or foreign nationals to conduct business activities in Japan, they must generally choose one of the following three base forms. Each form is determined by comprehensively considering business objectives, scale, financial capacity, and legal requirements.

①Japanese Corporation (Subsidiary) Establishment

This method involves establishing a new Japanese corporation such as a joint-stock company (kabushiki-kaisha) or limited liability company (godo-kaisha). It is the most common and comprehensive entry form. The subsidiary becomes a legally independent entity separate from the foreign parent company, enabling completely independent business activities in Japan.

②Japanese Branch Office Setup

This method involves establishing a business office (branch) of a foreign corporation in Japan. It functions as part of the foreign corporation and is characterized by the ability to directly utilize the credibility of the home country corporation.

③Representative Office Establishment

This is a base for conducting preparatory activities toward future full-scale business development. It is limited to preparatory activities such as information gathering, market research, advertising and promotion, and goods procurement, and cannot conduct sales activities.

Detailed Explanation of Japanese Corporation (Subsidiary) Establishment

Establishing a Japanese corporation is the most reliable and credible method for foreign companies making full-scale entry into the Japanese market. Since it is established under Japanese law and has an independent corporate personality, it becomes a legally separate entity from the foreign parent company.

Major Advantages

Acquiring corporate status in Japan makes it easier to gain trust from business partners and financial institutions. Since official documents such as corporate registration certificates are issued, the company’s existence can be clearly proven. Bank account opening in the corporate name is possible, enabling smooth business commencement. As a completely independent business entity, contracts and various procedures can be conducted smoothly.

Disadvantages and Important Considerations

Capital is required for company establishment. Particularly when foreign nationals want to obtain “Business Manager” status of residence, capital of 30 million yen or more is required, and requirements such as employing one or more persons with Japanese language abilities, ①doctoral degree, master’s degree, or professional degree in management-related fields, ②3 years or more of management experience, etc., are expected to be required, necessitating strict condition fulfillment. Furthermore, business plans must undergo expert evaluation. Additionally, for joint-stock companies, legal fees alone require articles of incorporation certification fees and registration taxes. Moreover, since it is independent as a Japanese corporation, all rights and obligations belong to the Japanese corporation itself, and the foreign parent company bears no direct responsibility.

Tax Characteristics

Japanese corporations are treated as domestic corporations, so not only income earned in Japan but also worldwide income becomes subject to Japanese corporate tax. This is an important point that differs significantly from branch form.

Detailed Explanation of Japanese Branch Office Setup

A Japanese branch office is a business office established by a foreign corporation in Japan, functioning as part of the foreign corporation. Legally, it is considered the same entity as the foreign corporation, with the major characteristic of being able to directly utilize the credibility of the home country corporation.

Major Advantages

The credibility and brand power of the home country corporation can be directly utilized, making it particularly advantageous for companies with significant achievements in their home countries. Branch registration issues official documents and enables acquisition of certain credibility. Bank account opening in the branch name is also possible, enabling full-scale commencement of business activities.

Disadvantages and Restrictions

At least one Japanese resident must be appointed as “representative in Japan.” This is acceptable for foreigners living in Japan, but it is a mandatory requirement. Legal fees of 90,000 yen are required for business office establishment registration, or 60,000 yen even without establishing a business office. Additionally, when the home country corporation’s head office location or officers change, change registration is also required for the Japanese branch, creating ongoing management burdens.

Legal Position and Rights and Obligations

Japanese branches are merely business offices of foreign corporations and are legally considered the same business entity as the foreign corporation. The entity to which rights and obligations belong is the foreign corporation in the home country, and contracts concluded by the Japanese branch are also legally considered to have the foreign corporation as the contracting party.

Tax Treatment

Since branches are considered part of foreign corporations, the taxation target is limited to income earned in Japan, namely domestic source income. They are recognized as permanent establishments (PE) and their business income is taxed in Japan.

Detailed Explanation of Representative Office Establishment

A representative office is a base that conducts only preparatory activities toward future full-scale business development. It does not conduct sales activities and is limited to preparatory activities such as information gathering, market research, advertising and promotion, and goods procurement.

Major Advantages

Since registration is not required, no legal fees are incurred for establishment or setup. Activities in Japan can be started relatively quickly, and market research and preliminary preparations can be conducted at low cost.

Restrictions and Disadvantages

Direct sales activities such as contract conclusion with business partners cannot be conducted. Activities are limited to preparatory activities only. Since there are no official documents, it may be difficult to gain trust from business partners. Obtaining status of residence for foreign representatives and employment of Japanese staff is often relatively difficult, and corporate bank accounts cannot be opened, requiring use of the representative’s personal account (it is possible to include the office name as a trade name).

Tax Characteristics

Representative offices generally do not constitute permanent establishments (PE), so Japanese corporate tax is not imposed. However, if the actual activities are judged to be conducting sales activities, there is a risk of being recognized as PE and being subject to corporate tax retroactively.

Attribution of Rights and Obligations

Representative offices are not legally recognized as business entities. Rights and obligations basically belong to the foreign corporation in the home country, but when representatives conclude contracts in their personal names, those individual representatives may become the entities to which rights and obligations belong.

The Concept of Permanent Establishment (PE) and Its Tax Importance

Permanent Establishment (PE) refers to a fixed place of business and is an extremely important concept for determining whether foreign corporations have obligations to pay corporate tax in Japan.

In international tax rules, there is a principle of “no taxation without PE,” meaning foreign corporations are not taxed on their business income in Japan unless they have PE in Japan. Specifically, branches, offices, and factories correspond to PE.

Representative offices usually do not constitute PE and are therefore non-taxable, but if they conduct sales activities, there is a risk of being recognized as PE and being taxed. On the other hand, branches are considered PE from the beginning, so business income in Japan becomes taxable.

Scope of Taxable Income: Domestic Source Income and Worldwide Income

The most important tax difference in choosing an entry form is the scope of income subject to taxation.

| Entry Form | Taxable Income | Explanation |

|---|---|---|

| Representative Office | Generally None | Not subject to taxation as no sales activities are conducted |

| Japanese Branch | Domestic Source Income | Only income arising from business activities within Japan |

| Japanese Corporation | Worldwide Income | Income earned worldwide, regardless of Japan or overseas |

Domestic source income refers to income arising from business activities within Japan. In the case of branch form, only this domestic source income becomes subject to Japanese corporate tax.

Worldwide income refers to all income earned by the Japanese corporation worldwide, not just within Japan. In the case of subsidiary form, this worldwide income becomes the taxation target. If the subsidiary earns income overseas and corporate tax is also imposed in that country, international double taxation may occur. To prevent this, systems such as foreign tax credits are established.

Criteria for Selecting Entry Forms

To select the appropriate entry form, the following factors must be comprehensively considered.

Business Objectives and Scale

When the main purpose is market research or information gathering, representative offices are suitable. When conducting full-scale sales activities, choose branches or subsidiaries. When planning long-term, continuous business development, subsidiary establishment is advantageous.

Financial Capacity and Establishment Costs

When wanting to minimize initial costs, representative offices or branches are suitable. Subsidiary establishment requires capital (30 million yen or more for status of residence acquisition) and establishment fees.

Credibility and Social Recognition

When emphasizing credibility within Japan, subsidiaries with corporate status are most advantageous. When wanting to utilize home country credibility, branches are suitable.

Tax Impact

When considering overseas expansion, the tax burden may differ significantly between subsidiaries subject to worldwide income taxation and branches where only domestic source income is taxed.

Legal Responsibility and Risk Management

When emphasizing risk diversification from the parent company, subsidiaries with independent corporate status are suitable. In the case of branches, legal responsibility belongs to the foreign corporation in the home country.

Conclusion

Foreign company entry forms into Japan must be selected by comprehensively considering business objectives, scale, financial capacity, and tax strategy. Representative offices enable low-cost market research but cannot conduct sales activities. Branches can utilize home country credibility and only domestic source income is subject to taxation. Subsidiaries have the highest credibility and independence but are subject to worldwide income taxation.

Particularly important are the differences in the concept of permanent establishment (PE) and the scope of taxable income. These tax differences significantly impact long-term business strategy, so we recommend careful judgment after consulting with experts. By selecting the appropriate entry form, you can increase the probability of success in the Japanese market.