Basic Mechanism and Purpose of Transfer Pricing Taxation System

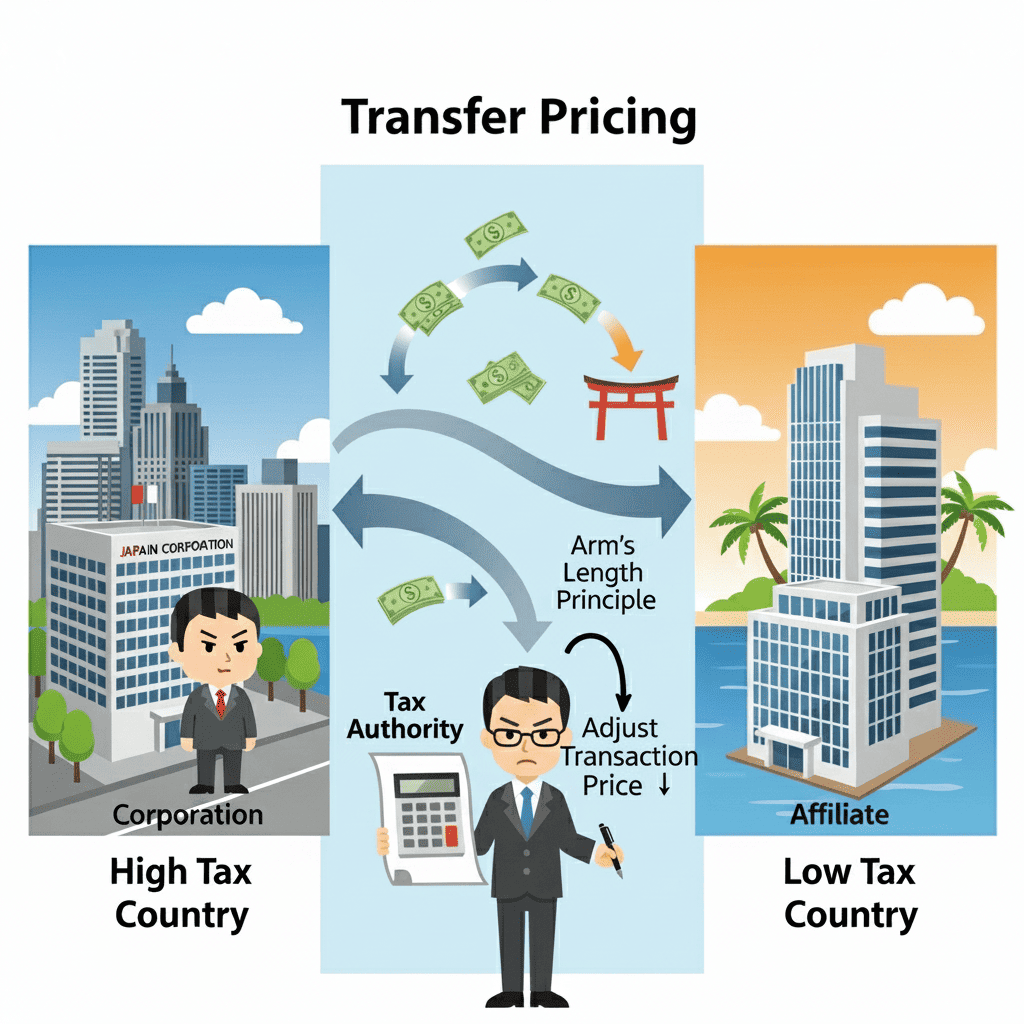

Transfer pricing taxation system is a system that recalculates taxable income based on appropriate prices when income is transferred overseas due to transaction prices between Japanese corporations and their foreign related companies (foreign related parties) differing from third-party transaction prices (arm’s length prices). The fundamental principle of this system is to prevent companies from intentionally manipulating intra-group transaction prices to concentrate profits in countries with low tax rates.

Let us explain with a specific example. Suppose Japanese parent company A sells products to overseas subsidiary company B at 110 yen, earning a profit of 10 yen. On the other hand, when selling the same product to a third party, the price would be 150 yen, resulting in a profit of 50 yen. This 40 yen difference becomes the issue, and for tax purposes, the taxable income is recalculated as if the transaction occurred at 150 yen.

This system was introduced in Japan in 1986 (Showa 61) and is developed in accordance with OECD (Organisation for Economic Co-operation and Development) guidelines. The purpose of the system can be summarized into the following three points:

First, to prevent companies from intentionally transferring profits to countries with low tax rates. Second, to secure tax revenue for each country. Third, to achieve fair tax burden. Through these objectives, it functions as a common standard for preventing international double taxation.

Concept and Importance of Arm’s Length Price

Arm’s length price refers to the price that would be charged between unrelated third parties under the same conditions. This is a core concept of transfer pricing taxation system and serves as the standard for judging the appropriateness of transactions between related companies.

Why is this price important? In transactions between related companies, normal market competition principles often do not function effectively, which may result in prices that cannot be considered fair. Arm’s length price is regarded as the most objective and fair price as it reflects market competition principles.

Determining arm’s length price requires the following process: searching for comparable third-party transactions, comparing transaction conditions (product content, quantity, payment terms, etc.), analyzing functions, risks, and assets, and selecting appropriate calculation methods.

There are also practical difficulties. Finding third-party transactions under completely identical conditions is challenging, and it becomes particularly complex in the case of intangible assets (patents, trademarks, etc.). Additionally, differences in economic environment and market conditions must be considered.

Definition of Foreign Related Parties and Special Relationships

Foreign related parties refer to foreign corporations and other entities that have special relationships with the corporation, such as shareholding relationships of 50% or more. This definition is an important element that clarifies the scope of application of transfer pricing taxation system.

Specific relationships include the following: parent and subsidiary relationships (50% or more investment), relationships between subsidiaries (having the same parent company), and other controlling relationships. The reason for the 50% standard is that this is the level at which substantial influence can be exercised over management, it aligns with international standards, and it provides an objective and clear judgment criterion.

For example, if Japanese company A holds 60% of the shares of American company B, then B becomes a foreign related party of A. Also, if both Japanese company C and Singaporean company D are 100% subsidiaries of company E, then C and D become mutual foreign related parties.

The types of transactions covered are diverse: buying and selling of goods, provision of services, lending of funds, licensing of intangible assets, and all other transactions are included.

Background of BEPS Project and Its Impact on International Taxation

BEPS is an abbreviation for “Base Erosion and Profit Shifting,” a project launched by the OECD Tax Committee in June 2012. This project was a groundbreaking initiative to comprehensively review international tax rules to respond to structural changes in global economic activities.

The background for launching the BEPS project included several serious problems. The business models of multinational enterprises became increasingly complex and globalized, the development of the digital economy created discrepancies with existing international tax rules, and the limited information-gathering capabilities of national tax authorities made it difficult to understand the actual situation of companies.

Specific problems included multinational enterprises transferring profits to countries with low tax rates, misalignment between actual business activities and income generation locations, excessive tax planning utilizing differences in tax systems of various countries, and widening information gaps between tax authorities and companies.

The project’s objectives are structured around three pillars: establishing a level playing field to create an environment where all companies can compete under the same conditions, improving transparency to enable tax authorities to understand the actual activities of companies, and modernizing international tax rules to create rules adapted to current business models.

Three Pillars of Transfer Pricing Documentation System

The BEPS project final report (October 2015) recommended the creation and provision of three types of documents to improve corporate transparency. These documents are important tools for tax authorities to comprehensively understand the activities of multinational enterprises.

(A) Local File is a document that records detailed information for calculating arm’s length prices in transactions between domestic companies and foreign related parties. Specific items to be recorded include transaction content, function and risk analysis, profit and loss statements, and arm’s length price calculation methods. The purpose is to enable each country’s tax authorities to conduct transfer pricing investigations efficiently.

(B) Country-by-Country Report is a document that records information on the allocation of revenue and tax payments by country for multinational enterprise groups. Specific items to be recorded include sales, pre-tax profits, taxes paid, and number of employees in each country. The purpose is to understand the overall activity status of corporate groups and utilize it for risk assessment.

(C) Master File is a document that records information about the overall picture of multinational enterprise groups, including organizational, financial, and business overviews. Specific items to be recorded include organizational structure, business content, intangible assets, financial transactions, and financial condition. The purpose is to provide basic information about corporate groups and identify transfer pricing risks.

The relationship between these three documents can be organized as follows: the Master File serves as a map of the entire corporate group, the Country-by-Country Report provides an overview of activities in each country, and the Local File provides detailed analysis of specific transactions.

Details of Simultaneous Documentation Obligations in Japan

In Japan, simultaneous documentation obligations were introduced through the 2016 tax reform. This is a system that requires the creation and preservation of Local Files by the deadline for submitting final tax returns. The meaning of “simultaneous” is that documentation should be performed at the same time as setting transaction prices, and post-hoc creation is considered insufficient.

Application requirements apply when any of the following conditions are met: the total amount of transactions with one foreign related party in the previous fiscal year was 5 billion yen or more, or the total amount of intangible asset transactions was 300 million yen or more.

The content of documents to be created falls into two categories. For documents describing the content of transactions with foreign related parties, it is necessary to record the content of assets and services related to transactions, functions and risks fulfilled by the corporation and foreign related parties, profit and loss details of the corporation and foreign related parties, business content, and business policies. For documents for calculating arm’s length prices, it is necessary to record arm’s length price calculation methods, reasons for selecting those methods, methods for selecting comparable transactions, and details of comparable transactions.

The application starts from fiscal years beginning on or after April 1, 2017 (Heisei 29), and applicable companies are required to respond reliably.

Obligations to Provide CbC Reports and Master Files

Large multinational enterprise groups are obligated to provide CbC Reports and Master Files. The scope of application covers multinational enterprise groups whose ultimate parent company’s consolidated total revenue in the immediately preceding accounting year was 100 billion yen or more.

The content of CbC Reports (Country-by-Country reporting matters) is very detailed, requiring the recording of revenue amounts, pre-tax current profits, taxes paid, taxes incurred, capital amounts, retained earnings amounts, number of employees, and tangible assets (other than cash and cash equivalents) for each country and region.

For Master File content (business overview reporting matters), it is necessary to record the organizational structure of multinational enterprise groups, business overview, content of intangible assets, intra-group financial transactions, and financial and tax positions.

Regarding provision methods and deadlines, documents must be provided to the competent tax office director through e-Tax (National Tax Electronic Filing and Payment System), with a deadline of within one year from the day following the end of the ultimate parent company’s accounting year. The application starts from accounting years of ultimate parent companies beginning on or after April 1, 2016 (Heisei 28).

An important note is that Country-by-Country Reports are clearly positioned as tools for risk assessment and statistics, not for income allocation. This means that simply allocating income to each country based on Country-by-Country Report data is not appropriate.

Efforts to Resolve Information Asymmetry

One of the most important issues that the BEPS project aimed to solve was the significant information asymmetry between multinational enterprises and national tax authorities. While multinational enterprises operate worldwide, national tax authorities can only understand corporate activities within their own countries, creating a significant information gap.

Due to this information gap, the profit allocation and activity reality of entire companies became opaque, making it difficult for tax authorities to impose appropriate taxation. For example, while companies could see “the entire forest,” tax authorities could only see “a single tree.”

The BEPS project recommended establishing mechanisms for countries to cooperatively share information to resolve this information asymmetry. This enables tax authorities in each country to comprehensively understand the overall activity status and income allocation of multinational enterprise groups, making it possible to more effectively monitor and prevent tax avoidance behaviors.

By requiring companies to comprehensively disclose group-wide information through Country-by-Country Reports (CbC Reports) and other means, the aim was to enable tax authorities in each country to understand “the entire forest.” This is highly evaluated as a groundbreaking initiative for improving transparency in international taxation.

Conclusion

Transfer pricing taxation system and the BEPS project represent important institutional reforms for achieving fair and transparent international taxation in increasingly globalized economic activities. The transfer pricing taxation system, introduced in 1986, has appropriately monitored international transactions of companies based on the concept of arm’s length price.

The BEPS project, launched in 2012, established three documentation systems—Local Files, Country-by-Country Reports, and Master Files—to resolve information gaps between multinational enterprises and tax authorities and address issues of base erosion and profit shifting. In Japan, these systems were also established through the 2016 tax reform, imposing new compliance obligations on companies.

International tax rules are expected to continue developing in the future. It is important for corporate executives and tax personnel to correctly understand these systems and take appropriate measures to achieve both sound business activities and tax compliance. Through improved transparency and the realization of fair competitive environments, contribution to sustainable global economic development is expected.