Japan Export Tax Exemption for Consumption Tax

The export tax exemption system is based on the fundamental principle that consumption tax, being a domestic consumption tax, should not be imposed on goods and services consumed abroad. Consumption tax is exempted for four types of export transactions conducted by taxable business operators: exports from Japan, international communications and postal services, transfer or lending of intangible property rights to non-residents, and provision of services to non-residents. However, services provided to non-residents that involve direct benefits enjoyed domestically are not subject to tax exemption and remain taxable. Tax exemption application requires preservation of supporting documents according to transaction types for seven years, and input tax credits are available for taxable purchases corresponding to export transactions. This system enhances Japan’s export competitiveness and prevents double taxation burden.

Scope of Export Transactions Subject to Tax Exemption

When taxable business operators conduct the following export transactions, consumption tax is exempted:

(1) Transfer or lending of assets conducted as exports from Japan

(2) International communications, postal services, or correspondence delivery between domestic and foreign locations

(3) Transfer or lending of intangible property rights such as mining rights, industrial property rights, copyrights, and business rights to non-residents

(4) Provision of services to non-residents

However, even for services provided to non-residents, those involving transportation or storage of domestically located assets, domestic dining or accommodation, and other similar services where the non-resident directly enjoys benefits domestically are not considered exempt export transactions and are subject to consumption tax.

(Note) “Non-residents” here refers to natural persons who do not have an address or residence in Japan and corporations that do not have their principal office in Japan. Notably, branches, representative offices, and other offices of non-residents in Japan are deemed residents regardless of their legal authority to represent, even when their principal office is located abroad.

What Constitutes Export Transactions

The export tax exemption system is based on the extremely important principle that “consumption tax, being a domestic consumption tax, should not be imposed on goods consumed abroad.”

Basic Concept: Consumption tax is imposed on domestic consumption. For example, when a product manufactured in Japan is exported to the United States, that product will be consumed in the United States, making it inappropriate to impose Japan’s consumption tax. If Japan imposes consumption tax and the United States also imposes value-added tax or similar taxes, the same product would bear a double tax burden.

Specific examples:

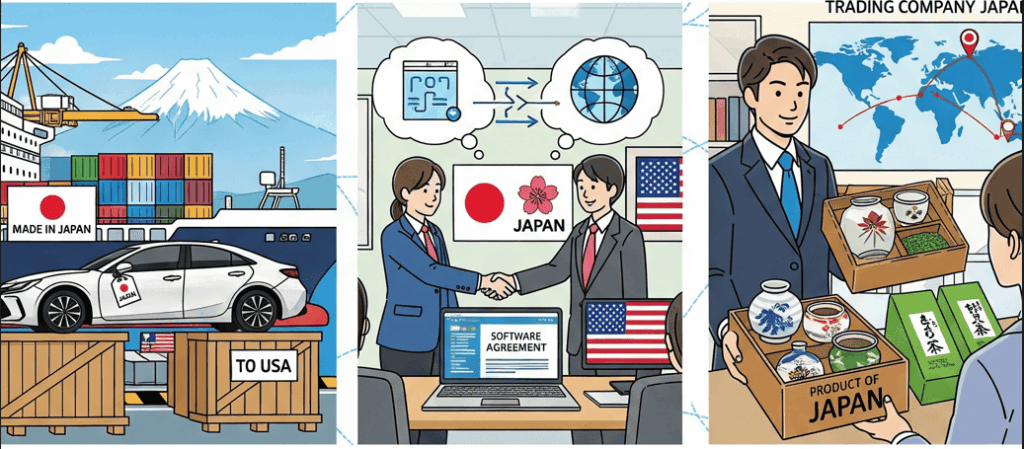

- When an automobile manufacturer exports cars manufactured in Japan to the United States

- When a software company licenses programs developed in Japan to overseas companies

- When a trading company sells domestically procured goods to overseas customers

All of these qualify as export transactions exempt from consumption tax, maintaining international competitiveness and preventing double taxation.

Four Categories of Export Transactions Subject to Tax Exemption

Export transactions subject to tax exemption are clearly classified into four categories by law.

(1) Transfer or lending of assets conducted as exports from Japan

This represents the most common type of export transaction, involving physical goods shipped abroad.

Examples: Export of machinery and equipment, export of agricultural products, export of used vehicles

Lending examples: Leasing construction machinery to overseas construction sites

(2) International communications, postal services, or correspondence delivery between domestic and foreign locations

This covers international information transmission services.

Examples: International telephone services, international internet communications, international postal services

Modern applications primarily include satellite communications and internet communications

(3) Transfer or lending of intangible property rights such as mining rights, industrial property rights, copyrights, and business rights to non-residents

This covers transactions involving intangible property rights.

Examples: Patent licensing, trademark transfers, copyright licensing

Software usage rights and brand usage rights are also included

(4) Provision of services to non-residents

This covers service provision to overseas customers.

Examples: Consulting services, design work, translation services

However, important exceptions apply (discussed later)

Definition of Non-Residents and Judgment Criteria

The definition of “non-residents” is extremely important in tax law and is clearly established based on the Foreign Exchange and Foreign Trade Act.

Persons qualifying as non-residents:

For natural persons: Individuals without an address or residence in Japan

Examples: Americans residing in America, Japanese nationals residing in China

For corporations: Corporations without their principal office in Japan

Examples: American companies headquartered in America, Japanese companies headquartered in Singapore

Important Exception:

Even for non-residents, their Japanese branches or offices are “deemed residents.” This is a very important provision – even if the headquarters is overseas, transactions with Japanese branches are treated as domestic transactions and are not subject to export tax exemption.

Specific judgment examples:

Service provision to a Japanese branch of an American company → Provision to residents (taxable)

Service provision to the American headquarters of an American company → Provision to non-residents (exempt)

Supporting Documentation and Preservation Requirements for Tax Exemption

To receive export tax exemption, preservation of documents objectively proving that the transaction is genuinely an export transaction is required.

Importance of Supporting Documents:

These are necessary to prove the proper application of export tax exemption during tax audits. If documentation is inadequate, tax exemption measures may be denied.

Preservation Period and Location:

Preservation period: 7 years (long-term preservation is mandatory)

Preservation location: Tax domicile (principal office location or location notified to tax office)

Electronic Record Handling:

In response to modern digitization, electronic data preservation is also recognized. However, proper preservation methods must be maintained with the ability to output when necessary.

Relationship with Input Tax Credits

Input tax credits in the export tax exemption system are an important mechanism for optimizing business operators’ tax burden.

Basic structure:

Export sales: 0% consumption tax rate (exempt)

Taxable purchases: 10% (or 8%) consumption tax already paid

Result: Consumption tax paid on purchases is refunded

Specific calculation example: When goods are purchased for 800 yen (tax-exclusive) and exported for 1,000 yen (tax-exclusive)

At purchase: 800 yen + 80 yen consumption tax = 880 yen paid

At sale: 1,000 yen (0 yen consumption tax) = 1,000 yen received

At filing: 80 yen consumption tax paid is refunded (0 minus 80 yen = minus 80 yen)

Eligible taxable purchases:

Purchase costs of inventory goods

Office supplies necessary for export operations

Entertainment expenses, advertising costs

Other expenses related to export transactions

Value Standards and Required Documents for Postal Exports

Postal exports require different supporting documents depending on their value, creating a complex system.

Value judgment standards:

Standard amount: 200,000 yen (FOB price)

Judgment unit: Principally per postal item

Split shipments to same recipient: Judged by total amount

FOB price definition:

“Free on Board” price, meaning the value under FOB delivery terms. Practically, this is the sales amount (amount received by the exporter).

Over 200,000 yen:

Export permit (document certified by customs director) required

Same procedures as regular export cargo are required

200,000 yen or less:

Further categorized by type of postal item

Parcel post/EMS: Japan Post acceptance certificate + shipping slip copy

Regular mail: Japan Post acceptance certificate (with item names, quantities per item, and values per item added)

Terminology

Domestic consumption tax: Tax imposed on domestic consumption. Consumption tax has this nature, making taxation on exported goods inappropriate

FOB price: Free on Board price. One of the Incoterms where the seller bears costs until goods are loaded onto the ship

Non-resident: Defined under Foreign Exchange Law as natural persons without address/residence in Japan or corporations without principal office in Japan

Taxable purchases: Transactions where business operators pay consumption tax when purchasing goods or services. When consumption tax is paid for export-exempt transactions, this consumption tax may become eligible for refund

Input tax credit: System allowing deduction of consumption tax paid on purchases from consumption tax on sales

Qualified invoice: Official invoice under the invoice system meeting specific requirements and issued by registered business operators

Universal Postal Convention: International treaty concerning international postal services, defining types of postal items (parcels, EMS, regular mail)

Exclusion of Services Where Direct Benefits are Enjoyed Domestically

Not all services provided to non-residents qualify for tax exemption. Services where direct benefits are enjoyed domestically remain taxable.

Examples of taxable (non-export exempt) service provision:

Transportation/storage services: Domestic product delivery, domestic warehouse storage

Dining/accommodation services: Domestic hotel accommodation, domestic restaurant meals

Other services where direct benefits are enjoyed domestically: Domestic event planning, domestic real estate management

Judgment criteria:

The location of service provision and where benefits are enjoyed are important judgment factors. When non-residents come to Japan and directly receive services, this is considered domestic consumption and therefore taxable.

Comparative examples:

Exempt: Management consulting for overseas companies (benefits enjoyed overseas)

Taxable: Domestic training services for visiting overseas company executives (benefits enjoyed domestically)

Specific Scope of Export Tax Exemption (Based on Basic Circular 7-2-1, Partially Excerpted and Modified)

The specific scope of export tax exemption is described in Consumption Tax Law Basic Circular 7-2-1. (Partially excerpted and modified)

7-2-1 The scope of export tax exemption under Article 7, Paragraph 1 of the Consumption Tax Law and each paragraph of Article 17 of the Consumption Tax Law Enforcement Order should be noted as approximately as follows.

(1) Transfer or lending of assets conducted as exports from Japan (principally referring to exports as defined in Article 2, Paragraph 1, Item 2 of the Customs Law)

(2) Transfer or lending of foreign goods

(3) Transportation of passengers or cargo conducted between domestic and foreign locations (including domestic transport sections conducted as part of international transport)

(4) Transfer or lending of international vessels, etc. (vessels or aircraft used exclusively for passenger or cargo transport between domestic and foreign locations or between foreign locations) to vessel operators, etc.

(Note) International vessels, etc. include Japanese-flagged vessels or aircraft.

(5) Repair of international vessels, etc. at the request of vessel operators, etc.

(6) Transfer or lending of containers used exclusively for cargo transport between domestic and foreign locations or between foreign locations to vessel operators, etc., or repair of such containers at the request of vessel operators, etc.

(7) Service provision for pilotage, guidance, and other assistance for entry/departure or takeoff/landing of international vessels, etc., or provision of facilities for entry/departure, takeoff/landing, berthing, or parking to vessel operators, etc.

(8) Service provision for stevedoring, transport, storage, tallying, or surveying of foreign goods

(Note) For these services related to special export goods (as defined in Article 30, Paragraph 1, Item 5 of the Customs Law), only the following are included:

(1) Those conducted in designated bonded areas, etc. and at loading locations onto vessels or aircraft for export of such special export goods

(2) Transport between designated bonded areas, etc.

(9) Communications, postal services, or correspondence delivery between domestic and foreign locations

(10) Transfer or lending to non-residents of intangible fixed assets, etc. listed in Article 6, Paragraph 1, Items 4 to 8 of the Consumption Tax Law Enforcement Order

(11) Service provision to non-residents other than the following:

a. Transportation or storage of domestically located assets

b. Dining or accommodation in Japan

c. Services similar to a or b where direct benefits are enjoyed domestically

Legal Basis (Partially Excerpted and Modified by Author)

Consumption Tax Law Article 7

(Export Tax Exemption, etc.)

Article 7: For taxable transfers of assets, etc. conducted domestically by business operators (excluding those exempt from consumption tax payment obligation) that fall under the following categories, consumption tax shall be exempted.

1. Transfer or lending of assets conducted as exports from Japan

2. Transfer or lending of foreign goods (excluding those falling under the previous item, etc.)

3. Transportation of passengers or cargo or communications conducted between domestic and non-domestic areas

4. Transfer, lending, or repair of vessels or aircraft used exclusively for transport specified in the previous item, as prescribed by government ordinance

5. Those prescribed by government ordinance as similar to transfers of assets, etc. listed in the previous items

Paragraph 2: The provisions of the previous paragraph shall not apply when proof that the taxable transfer of assets, etc. falls under transfers of assets, etc. listed in each item of the same paragraph is not provided as prescribed by Ministry of Finance ordinance.

Consumption Tax Law Enforcement Order Article 17

(Scope of Export Transactions, etc.)

Article 17: The transfer, lending, or repair of vessels or aircraft prescribed by government ordinance in Article 7, Paragraph 1, Item 4 of the Consumption Tax Law shall be as follows:

1. Transfer or lending of vessels specified in Item 4 of Article 7, Paragraph 1 of the Law to those engaged in vessel operation business as prescribed in Article 2, Paragraph 2 of the Maritime Transport Law or vessel leasing business as prescribed in Paragraph 10 of the same Article

2. Transfer or lending of aircraft specified in Item 4 of Article 7, Paragraph 1 of the Law to those engaged in air transport business as prescribed in Article 2, Paragraph 18 of the Aviation Law

3. Repair of vessels specified in Item 1 or aircraft specified in the previous item at the request of persons specified in Item 1 or the previous item

Paragraph 2: Those prescribed by government ordinance in Article 7, Paragraph 1, Item 5 of the Law shall be the following transfers of assets, etc.:

1. Transfer, lending, or repair of vessels or aircraft used exclusively for passenger or cargo transport between non-domestic areas as follows:

a. Transfer or lending of vessels to those engaged in vessel operation or vessel leasing business

b. Transfer or lending of aircraft to those engaged in air transport business

c. Repair of vessels or aircraft at the request of persons specified in a or b

2. Transfer or lending of containers used exclusively for cargo transport between domestic and non-domestic areas or between non-domestic areas to those engaged in vessel operation, vessel leasing, or air transport business, or repair of such containers at the request of vessel operators, etc.

3. Service provision for pilotage, guidance, and other assistance for entry/departure or takeoff/landing of aircraft specified in Item 1 of the previous paragraph, or provision of facilities for entry/departure, takeoff/landing, berthing, or parking (including lending of such facilities), and other similar service provision to vessel operators, etc.

4. Service provision for stevedoring, transport, storage, tallying, surveying, and other similar services related to foreign goods (including these services related to goods to be exported and imported goods that have received import permission in designated bonded areas as prescribed in Article 29 of the Customs Law, and for these services related to special export goods as prescribed in Article 30, Paragraph 1, Item 5 of the same Law, limited to those conducted in designated bonded areas, etc. and at loading locations onto vessels or aircraft for export of such special export goods, and transport between designated bonded areas, etc.)

5. Postal services or correspondence delivery conducted between domestic and non-domestic areas

6. Transfer or lending of assets listed in Items 4 to 8 of Article 6, Paragraph 1 to non-residents

7. Service provision to non-residents other than those listed in Items 3 and 1 to 5 of the previous paragraph and Article 7, Paragraph 1, Item 3 of the Law, except for the following:

a. Transportation or storage of domestically located assets

b. Dining or accommodation in Japan

c. Services similar to a and b where direct benefits are enjoyed domestically

Paragraph 3: Lending of money as prescribed in Article 10, Paragraph 1 or acts listed in Items 1, 2, or 5 to 8 of Paragraph 3 of the same Article where the debtor of monetary claims related to such lending or acts (limited to those who received discounts for Item 7 of the same paragraph) is a non-resident, and lending of assets listed in Item 11 of the same paragraph to non-residents shall be deemed as those prescribed by government ordinance in Article 7, Paragraph 1, Item 5 of the Law for the application of Article 31, Paragraph 1 of the Law.